WASHINGTON, D.C. (July 18, 2018) –

The Mortgage Bankers Association’s Market Composite Index, a measure of mortgage loan application volume, decreased 2.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 22 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index increased 19 percent compared with the previous week and was 1 percent higher than the same week one year ago.

The refinance share of mortgage activity increased to 36.5 percent of total applications from 34.8 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 6.1 percent of total applications.

The FHA share of total applications increased to 10.6 percent from 10.0 percent the week prior. The VA share of total applications decreased to 10.2 percent from 11.3 percent the week prior. The USDA share of total applications decreased to 0.7 percent from 0.8 percent the week prior.

National Average of Interest Rates

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) increased to 4.77 percent from 4.76 percent, with points increasing to 0.46 from 0.43 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $453,100) decreased to 4.66 percent from 4.68 percent, with points increasing to 0.30 from 0.24 (including the origination fee) for 80 percent LTV loans.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA decreased to 4.78 percent from 4.80 percent, with points decreasing to 0.69 from 0.75 (including the origination fee) for 80 percent LTV loans.

The average contract interest rate for 15-year fixed-rate mortgages increased to 4.22 percent from 4.18 percent, with points decreasing to 0.42 from 0.46 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

Refinancing or Buying-

We monitor real time interest rates, so our clients are able to access some of the lowest rates available.

Buying or Refinancing a home doesn’t have to be Stressful. With rates still historically low, poised to move higher, many would be home buyers are moving quickly to finance their piece of the American Dream. Existing home owners have refinanced at least once, even twice. But there are still many who have not, due to either not wanting to deal with the stress of gathering documents and not sure of qualifying for a loan.

At North Atlantic you receive attentive personalized service

(see what our clients say).

Believe me it’s a great deal easier with our help and expertise. The average time to close a loan is about 30 days. We understand the guidelines and know what different lenders can do, which increases your opportunities for a fast easy loan with a great rate.

Don’t put it off any longer and start saving with a lower mortgage payment.

There’s no salesman to speak with only qualified mortgage experts.

For a Free Consultation:

Call or Email:

John Sauro

Ph: 877-794-5363

Email: JohnSauro@Gmail.com

Powell backs more rate hikes as economy growing ‘considerably stronger’

The U.S. economy is running at a fast enough pace to justify continued interest rate increases, Federal Reserve Chairman Jerome Powell said Tuesday.

Powell is delivering his semiannual testimony to Congress this week, starting with an appearance Tuesday before the Senate Committee on Banking, Housing and Urban Affairs.

In remarks he provided ahead of a question-and-answer session, Powell painted a largely positive picture of the economy, which he said is expanding at an increasing pace and is being boosted by aggressive fiscal policy on Capitol Hill.

“Overall, we see the risk of the economy unexpectedly weakening as roughly balanced with the possibility of the economy growing faster than we currently anticipate,” Powell said.

“The unemployment rate is low and expected to fall further. Americans who want jobs have a good chance of finding them,” he added.

Powell spoke as the central bank is in the process of gradually raising interest rates. The policymaking Federal Open Market Committee has hiked the Fed’s benchmark rate twice this year in quarter-point increments, and is expected to approve two more increases before the end of the year.

Though the economy grew at just a 2 percent pace in the first quarter, Powell said growth in the second quarter was “considerably stronger than the first.”

“Robust job gains, rising after-tax incomes, and optimism among households have lifted consumer spending in recent months. Investment by businesses has continued to grow at a healthy rate,” he said. “Good economic performance in other countries has supported U.S. exports and manufacturing. And while housing construction has not increased this year, it is up noticeably from where it stood a few years ago.”

Inflation is running around the Fed’s 2 percent target for the first time in several years, while the unemployment rate is at 4 percent and consistent with a level that most economists consider near to full employment. Powell said wages are growing faster than a year ago but not enough to stoke inflation fears.

Powell made brief mention of the ongoing trade war between the U.S. and its global competitors, saying only that it is “difficult to predict” what the ramifications will be on the economy.

However, the “upbeat tone” from the testimony likely means the trade issues won’t keep the Fed from hiking rates, said Andrew Hunter, U.S. economist at Capital Economics.

House Buying at Near Historic Levels

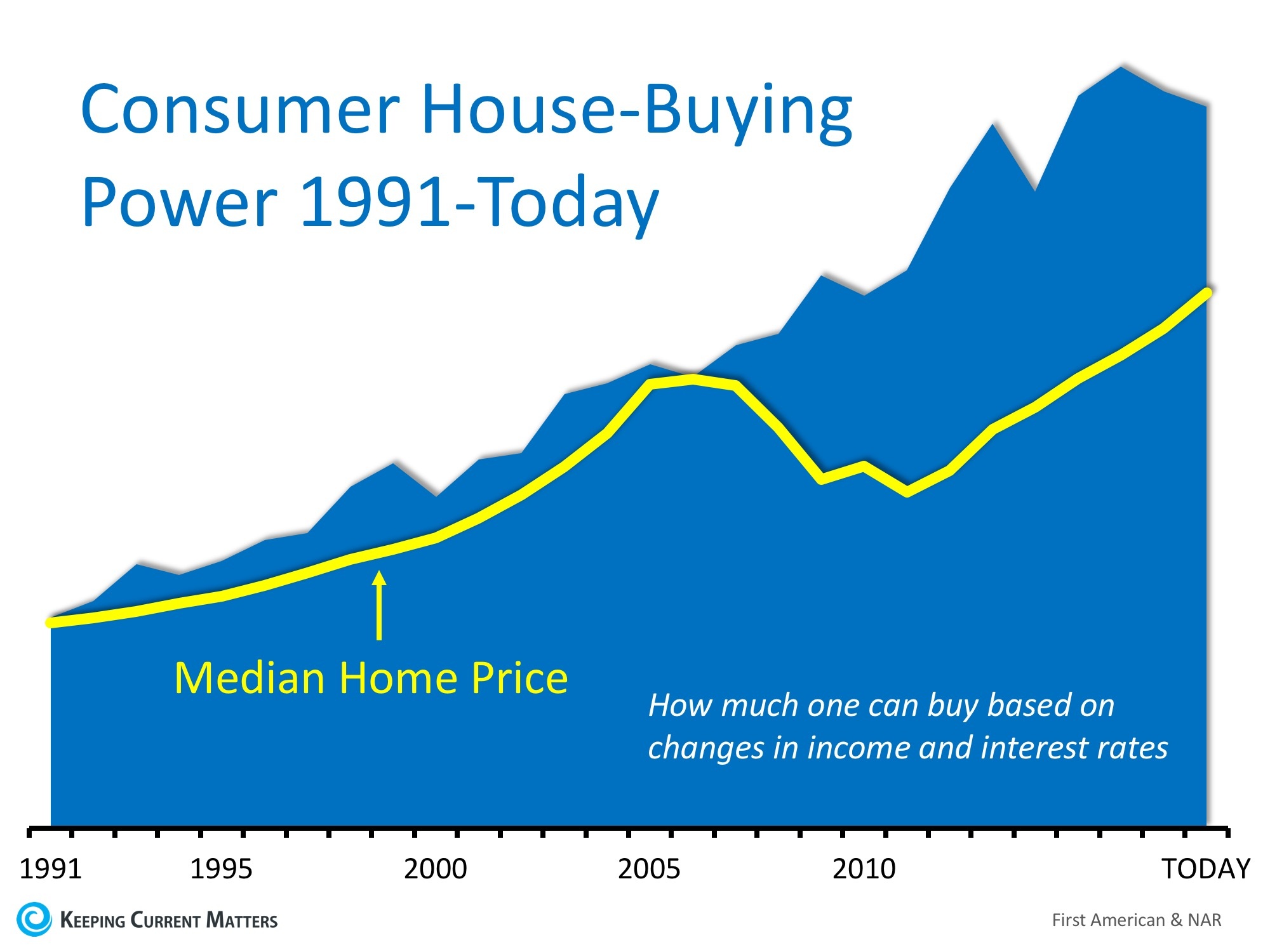

We keep hearing that home affordability is approaching crisis levels. While this may be true in a few metros across the country, housing affordability is not a challenge in the clear majority of the country. In their most recent Real House Price Index, First American reported that consumer “house-buying power” is at “near-historic levels.”

Their index is based on three components:

- Median Household Income

- Mortgage Interest Rates

- Home Prices

The report explains:

“Changing incomes and interest rates either increase or decrease consumer house-buying power or affordability. When incomes rise and/or mortgage rates fall, consumer house-buying power increases.”

Combining these three crucial pieces of the home purchasing process, First American created an index delineating the actual home-buying power that consumers have had dating back to 1991.

Here is a graph comparing First American’s consumer house-buying power (blue area) to the actual median home price that year from the National Association of Realtors (yellow line).

Consumer house-buyer power has been greater than the actual price of a home since 1991. And, the spread is larger over the last decade.

Bottom Line

Even though home prices are increasing rapidly and are now close to the values last seen a decade ago, the actual affordability of a home is much better now. As Chief Economist Mark Fleming explains in the report:

“Though unadjusted house prices have risen to record highs, consumer house-buying power stands at near-historic levels, as well, signaling that real house prices are not even close to their historical peak.”

Sources: MBA, NAR, Reuters