We are currently recommending Floating Mortgage Rates headed into the weekend as Bonds close near the highs.

Mortgage Rates had another crazy week, with intraday swings of one quarter to one half of a percent. Rates changed several times during each day of the past week. However, there are low rate opportunities; you just have to be able to lock the rate at that very moment and that’s difficult to do in this type of market. So, make sure you have your paperwork in so you can lock in when the time is right.

On Thursday, Mortgage Bonds continued to stabilize and move higher which moved Mortgage Rates lower, on dovish QE talk from several Fed members and also due to noted fund manager Jeffrey Gundlach saying he was bullish on the sector.

Mortgage Bonds managed to close near unchanged after a big drop earlier in the session closing at 101.47 up 3bp.

The Dow dropped 114.89 to 14,909.60, the S&P 500 fell by 6.92 points to 1,606.28 while the Nasdaq closed near unchanged at 3,403.25. For the quarter the Dow gained 2.2%, the S&P rose 2.3% and the Nasdaq was up 4.2%. Oil was last seen at $96.48/barrel down 58 cents. Next week is holiday shortened – the Bond markets will close early at 2:00pm ET on Wednesday and Stocks will close at 1:00pm. All capital markets will be closed on Thursday for 4th of July. Non-farm payrolls will be

released on Friday morning and it is expected that employers added 165K new jobs in June.

Economic Data confirmed the Fed will be active buyer of Bonds for a while, good for Mortgage Rates, as the Core Personal Consumption Expenditures (PCE) rose by just 0.1%, inline with estimates while year-over-year Core PCE was a scant 1.1%, well below the Fed’s upper end range of 2%.

Mortgage Rates Skyrocket on Fed Fears

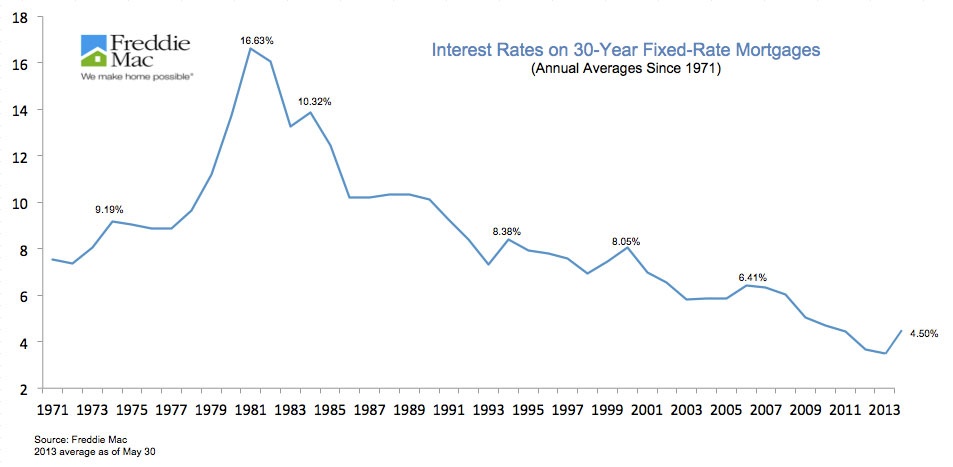

Mortgage Rates Rose last week on fears of less Fed intervention in the mortgage-bond market.

“Interest rates moved up sharply following the Federal Reserve press conference last Wednesday, June 19th, where it was indicated that the Fed could begin tapering their asset purchases later this year,” said Mike Fratantoni, MBA’s vice president of research and economics.

The 4.46% Fixed home loan rate that carries an additional 0.8 point/fees is up from 3.93% in the previous week. It was the largest weekly increase since 1987 and the highest it’s been since August 2011.

Fed In Overdrive Trying to Curb Rising Mortgage Rates

After this month’s Federal Open Market Committee minutes reached the public, the market took a hefty kick and mortgage rates surged higher. As a result, the Federal Reserve intensified its efforts to curb a growth-threatening rise in long-term interest rates, Bloomberg reports.

“It is pretty obvious that the Fed was caught off guard by the market’s reaction given the lengths to which they have gone to reshape market expectations,” Drew Matus, deputy U.S. chief economist at UBS Securities, said. “The range of both speakers and outlets suggests that these comments are, if not coordinated, then at least part of a collective — likely futile — effort to re-mold the market’s view of the June FOMC press conference.” Read the full story

Spiking Mortgage Rates Even with their recent rise, mortgage rates are still “incredibly low” by historical standards, so they will not halt the housing recovery, Trulia Chief Economist Jed Kolko told CNBC on Tuesday. Full Story

Tight Credit Is Slowing Housing Recovery

Tight credit, particularly for young people, is hindering the housing recovery, according to research published at the Joint Center For Housing Studies at Harvard University.

According to the State of the Nation’s Housing 2013 report, the recession has significantly boosted the rental market in the past several years. In 2012, the number of renter households in the U.S. increased by 1.1 million, and construction of new multifamily units increased at a double-digit rate.

However, this has come at the expense of the housing market.

Meanwhile, interest rates and home prices, although now on the rise, have hit historic lows, the unemployment rate is improving, inflation has stabilized, and the country’s economic picture has improved overall.

So why are so many young people still opting to rent?

As the study reveals, banks have tightened their lending standards, which in turn is preventing young people from buying homes. People age 25 – 54 saw their homeownership rates reach the lowest point in 2012 (record keeping began in 1976), according to the report.

“Tight credit is limiting the ability of would-be home buyers to take advantage of today’s affordable conditions and likely discouraging many from even trying,” says Chris Herbert, director of research at the Joint Center for Housing Studies. “At issue is whether, and at what cost, mortgage financing will be available to borrowers across a broad spectrum of incomes, wealth and credit histories moving forward.”

Currently, more than 20.6 million households are spending more than half of their household income on housing, the report finds. And with so many homeowners struggling just to keep their homes, it could be that many younger people simply do not want to face the burden of having a mortgage.

Considering current economic conditions, the need for a strong rental market remains important, the research finds. However, federal budget sequestration will pare down the number of households receiving rental housing assistance.

“Given the profoundly positive impact that decent and affordable housing can have on the lives of individuals, families and entire communities, efforts to address these urgent concerns as well as longstanding housing affordability challenges should be among the nation’s highest priorities,” says Eric S. Belsky, managing director of the Joint Center for Housing Studies.

Housing News

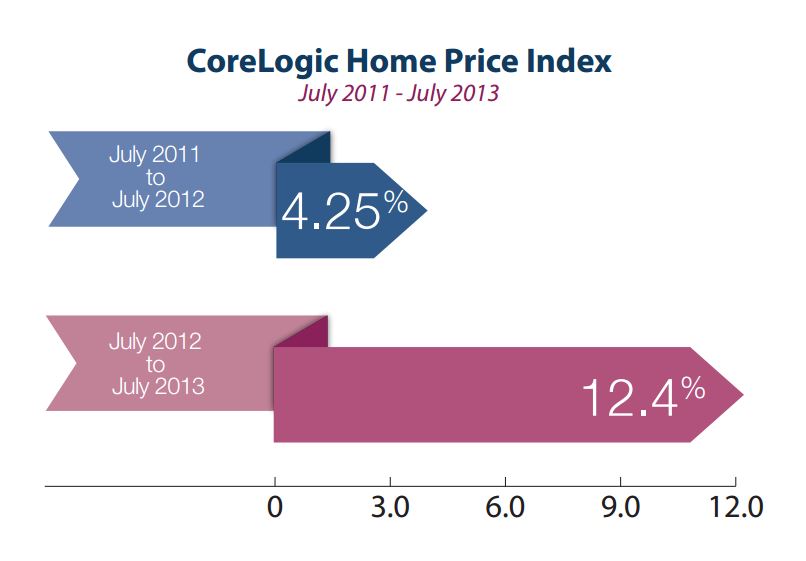

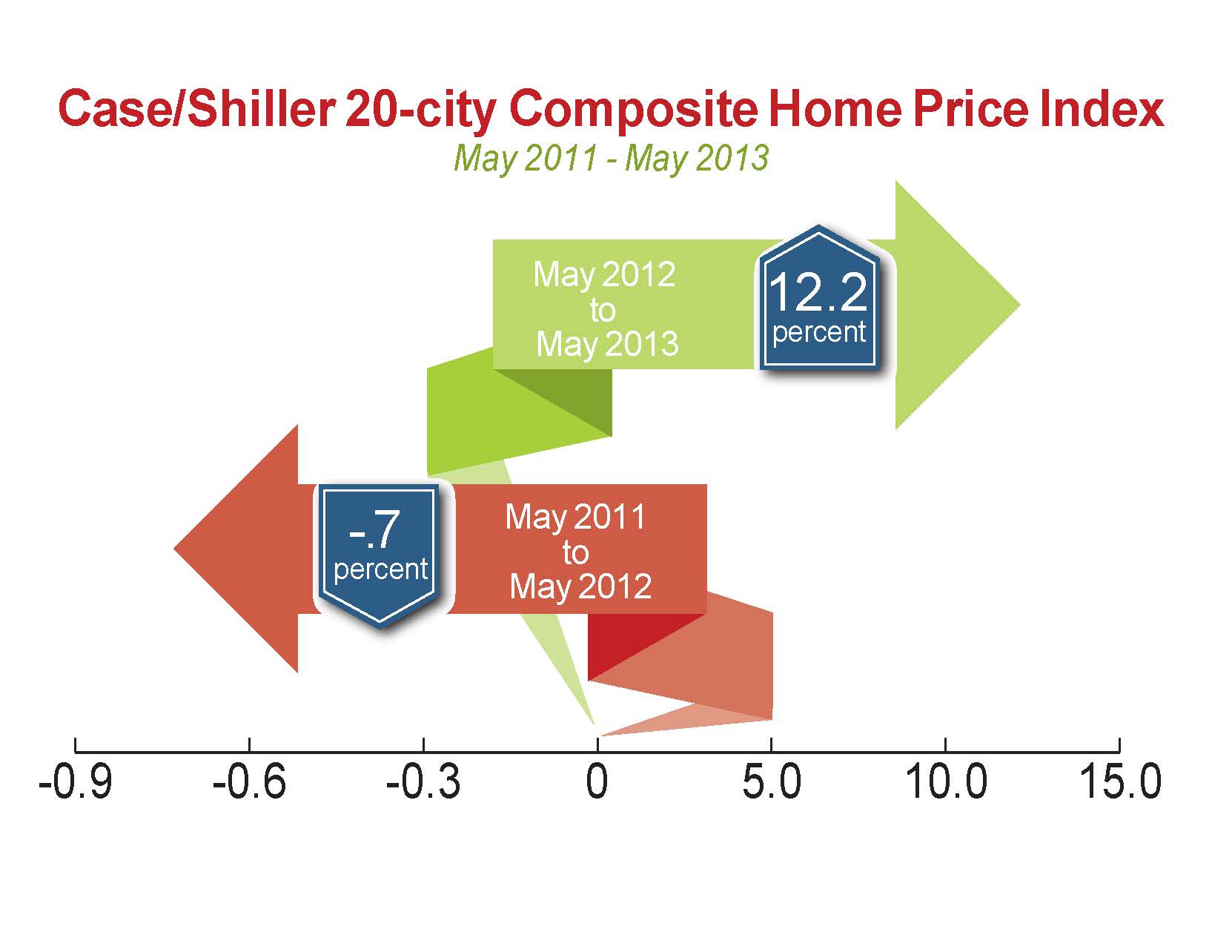

Home Prices took a major leap in April, setting a new monthly record for gains. From March to April, home price gained 2.6 percent and 2.5 percent for the top 10 and top 20 U.S. markets, respectively, according to the latest S&P/Case-Shiller Home Price Indices. Average prices rose 11.6 percent and 12.1 percent in April from a year ago.

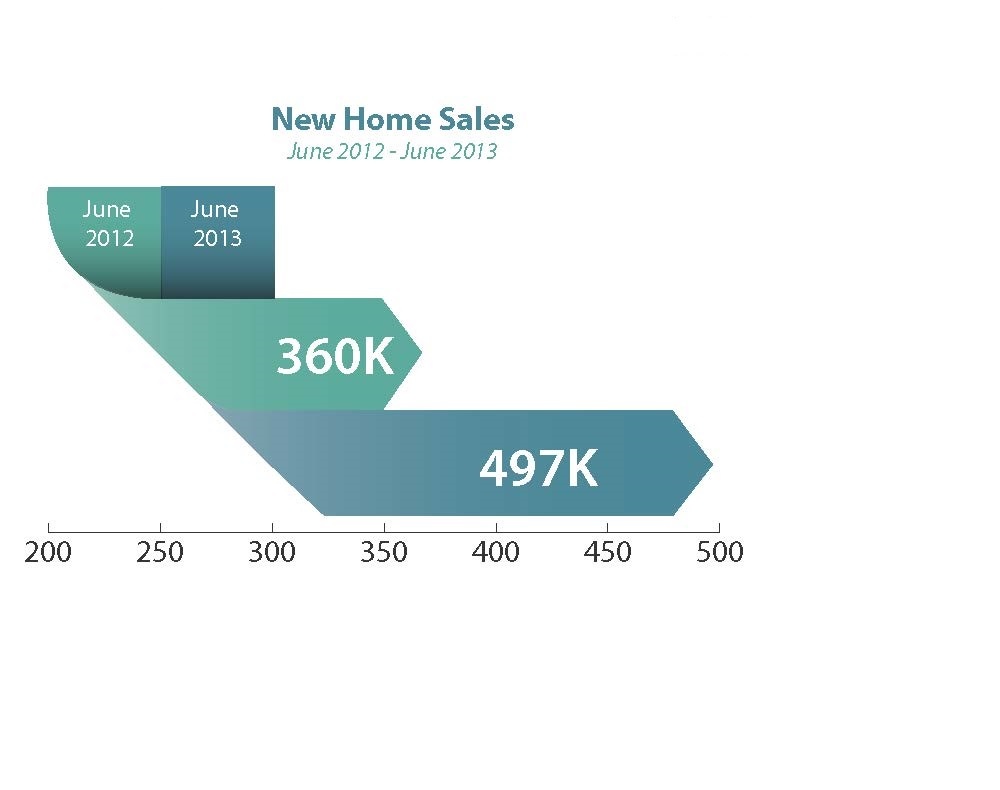

New Home Sales jumped to 476,000 in May, much higher than the 462,000 that analysts expected, according to the Commerce Department. Compared with May 2012, sales were up 29 percent. Home sales data will be closely watched in the coming months for signs of strain from the rise in mortgage rates. The housing market recovery, which is helping to soften the blow on the economy from tight fiscal policy, has been largely driven by record-low mortgage rates, thanks to the Federal Reserve’s generous monetary stimulus.

Pending Home Sales rise by 6.7%, above the 1.5% expected.

Spiking Mortgage Rates Even with their recent rise, mortgage rates are still “incredibly low” by historical standards, so they will not halt the housing recovery, Trulia Chief Economist

Jed Kolko told CNBC on Tuesday. Full Story

Economic News

U.S. orders for long-lasting goods rose a better-than-expected 3.6 percent in May, compared to a 3.5 percent increase the prior month. Economists polled by Reuters had expected goods orders to rise by 3.0 percent.

US consumer confidence rose to the highest level since January 2008.

First quarter Gross Domestic Product (GDP), came in at 1.8% versus expectations of 2.4%. The drop was attributed towards lower consumer spending and an pullback in business investment.

Weekly Jobless Claims fell 9,000 last week to a seasonally adjusted 346,000, according to the Labor Department, largely in line with expectations. The four-week moving average for new claims fell 2,750 to 345,750.

Consumer Spending rebounded 0.3 percent in May, matching estimates, after a revised 0.3 percent decline in the prior month, according to the Commerce Department.

Core Personal Consumption Expenditures (PCE) rose by just 0.1%, inline with estimates while year-over-year Core PCE was a scant 1.1%, well below the Fed’s upper end range of 2%.

Personal Spending rose by 0.3% in May after a 0.3% decline and was just below the 0.4% expected. Personal Incomes jumped by 0.5% versus the 0.2% anticipated.

The Personal Savings rate moved up to 3.2% from 3%

Consumer Sentiment at 84.1, above the 82.7 expected and up from the initial May reading of 82.7.

Chicago PMI falls to 51.6 in June from the My reading of 58.7 and below the 55.5 expected.

Sources: CNBC, Housingwire, MMG, Bloomberg, Mortgageorb