This week mortgage rates moved lower as the 4% Bond is nearing levels hit only twice this year. We will continue to float Mortgage Rates, not locking, but very cautiously. Rates are favorable, be careful as the technicals don’t give us any clear signs. Seeing this formation after an uptrend doesn’t mean you can sit back and take a vacation; for it does show indecision for Bonds.

Mortgage Bond prices rallied this week pushing Mortgage Rates lower, as Stocks were pressured on heavy selling as investors evaluated valuation levels against economic growth uncertainty. The major Stocks indexes had declines between 2.5% and 3.5%. This despite weekly initial jobless claims falling to near 7-yr lows. Today’s better than expected Consumer Sentiment capped Bond gains to a minimum, despite the plunge in Stocks. The 4% coupon closed at 104.59 up 6bp. Stocks fell as investors grow jittery and looked to secure profits. The Dow fell 143.47 points to 16,026.75, the S&P 500 lost 17.39 points to end at 1,815.69, while the tech heavy Nasdaq fell below 4,000 to end at 3,999.73 down 54.37 points. Oil was last seen at $103.37, closing near unchanged. Next week’s economic reports will touch on key sectors – housing, manufacturing, inflation and the job market (weekly claims).

U.S. Treasury Secretary Jack Lew told CNBC on Wednesday, by U.S. standards, we still have a lot of work to do to boost the economy. Read more

Fed minutes: Committee agreed 6.5% threshold was ‘outdated,’ vote to remove was unanimous

The members of the Federal Open Market Committee agreed unanimously in March that a 6.5 percent unemployment target for raising interest rates was ‘outdated’ and should be removed, according to Fed meeting minutes. Read more

Weekly Survey of Rates from the Mortgage Bankers Association

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) remained constant at 4.56 percent, with points increasing to 0.33 from 0.31 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $417,000) increased to 4.49 percent from 4.46 percent, with points decreasing to 0.14 from 0.27 (including the origination fee) for 80 percent LTV loans.

The average contract interest rate for 15-year fixed-rate mortgages remained constant at 3.62 percent, with points increasing to 0.31 from 0.23 (including the origination fee) for 80 percent LTV loans.

Commercial Real Estate Lending

Commercial Mortgage backed Securities (CMBS)– The 10 Yr Swap rate moved lower to finish the week at 2.798%, down from last weeks 2.80%.

Housing News

Three Reasons to Sell Your Home this Spring –by KCM

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are three of those reasons:

1. Demand is about to skyrocket

Most people realize that the housing market is hottest from April through June. The most serious buyers are well aware of this and, for that reason, come out in early spring in order to beat the heavy competition. We also have a pent-up demand as many buyers pushed off their home search this winter because of extreme weather. Sellers in markets where seasonal weather is never an issue must realize that buyers relocating to their region will increase dramatically this spring as these purchasers finally decide to escape the freezing temperatures of the winters in the north.

These buyers are ready, willing and able to buy…and are in the market right now!

2. There Is Less Competition – For Now

Housing supply always grows from the spring through the early summer. Also, there has been a growing desire for many homeowners to move as they were unable to sell over the last few years because of a negative equity situation. Homeowners have seen a return to positive equity as prices increased over the last eighteen months. Many of these homes will be coming to the market in the near future.

The choices buyers have will continue to increase over the next few months. Don’t wait until all the other potential sellers in your market put their homes up for sale.

3. There Will Never Be a Better Time to Move-Up

If you are moving up to a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 4% this year and 8% by the end of 2015. If you are moving to a higher priced home, it will wind-up costing you more in raw dollars (both in down payment and mortgage payment) if you wait. You can also lock-in your 30 year housing expense with an interest rate at about 4.5% right now. Freddie Mac projects rates to be 5.1% by this time next year and 5.7% by the fourth quarter of 2015.

Moving up to a new home will be less expensive this spring than later this year or next year.

Economic News

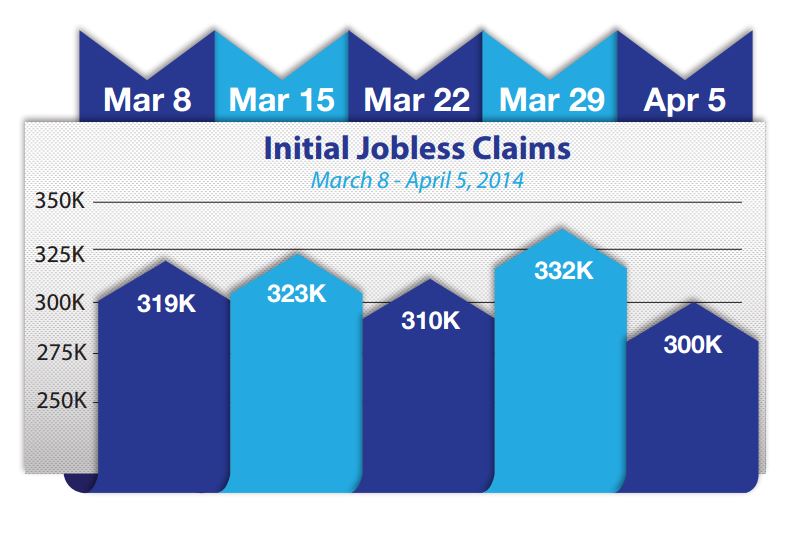

Happy days here again? Jobless claims tumble to near 7 year low

The number of Americans filing new claims for unemployment benefits fell sharply last week to the lowest level in almost seven years, which could bolster views of an acceleration in job growth after a cold winter dampened hiring. Initial claims for state unemployment benefits dropped 32,000 to a seasonally adjusted 300,000 for the week ended April 5, the lowest level since May 2007, the Labor Department said on Thursday. Claims for the week ended March 29 were revised to show 6,000 more applications received than previously reported. Read more

U.S. wholesale inventories rose at a slower pace in February than in the prior month, increasing 0.5 percent after a revised 0.8 percent gain in January, which could support views that restocking will not help the economy in the first quarter.

U.S. consumer credit rose more than expected in February, likely reflecting a surge in demand for student and automobile loans.

The Bank of England left its key interest rate unchanged at 0.5 percent and made no changes to its asset purchase target.

Consumer sentiment in the U.S. came in at 82.6. Economists had expected April’s advance reading of consumer sentiment to check in at 81.0, up slightly from March’s 80.0 reading.

Sources: CNBC, Bloomberg, MMG, Housingwire, MBA, KCM