Our thoughts and prayers go out to those who perished and survived the devastating tornado in Moore, Oklahoma.

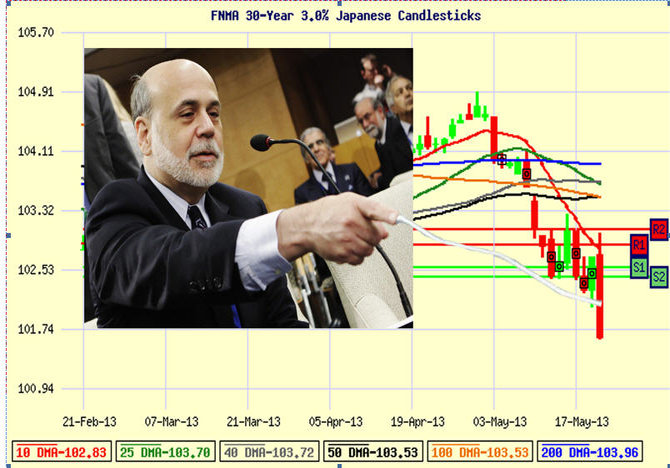

What a week for Mortgage Rates and Bond Prices. On Wednesday, an over reaction to Bernanke’s comments sent Mortgage Bond prices plunging. The Bonds were hit hard and about 5 times the magnitude of a typical trading day. By the time the day was over Bonds lost 106 basis Points in Price. Mortgage Rates, which move in the opposite direction moved higher. Bernanke was unclear as to whether the Fed will or will not pare back purchases. Bond Traders sold into the confusion and as technical support levels were broken, programmed trading kicked in which further exasperated the sell off. As evidenced by the sell off in Stocks – nobody won on Wednesday’s confusing Fed testimony.

Wednesday was another glaring example that technicals mean nothing when you get surprise news. The volatile trading action also reminds us that exiting QE3 may not be as smooth as they might think. Even though prices are at their worst levels in a year – the Bond is within just a few basis points of support (101.75) seen last August – and at that time, Bonds staged an amazing rally.

With Bonds and Mortgage Rates trying to stabilize, we currently recommend locking into rates in the short term days-weeks and floating longer term.

Bernanke Roils Markets

Mortgage Rates Move Higher for Second Straight Week

U.S. mortgage rates moved higher for a second consecutive week, with the benchmark 30-year fixed mortgage rate climbing to 3.71%, according to Bankrate.com‘s weekly national survey. The average 30-year fixed mortgage has an average of 0.34 discount and origination points, Bankrate.com adds.

The average rate for a 15-year fixed mortgage increased to 2.92%, while the average jumbo 30-year fixed rate inched lower to 3.99%. Rates for adjustable-rate mortgages (ARMs) also rose: Rates for five-year ARMs increased to 2.68%, while rates for 10-year ARMs climbed to 3.22%.

According to Bankrate.com, sudden “glass half-full” economic sentiment continues to push bond yields and mortgage rates higher, and the benchmark 30-year fixed mortgage rate is now the highest since early April.

Despite the increase, however, mortgage rates have been in a narrow one-third of a percentage point range since December, the company adds. The last time the average mortgage rate exceeded 5% was April 2011.

Housing News

Annual Home Value Appreciation Exceeds 5% for Sixth Straight Month

On a monthly basis, home prices increased 0.5% from March with the Zillow Home Value Index now at $158,300. Furthermore, annual home value appreciation exceeded 5% for the sixth straight month, as prices rose 5.2% year-over-year. The Seattle-based real estate information provider said this is the longest such streak since the height of the housing bubble in 2006.

Out of the 365 metropolitans analyzed by Zillow in this report, 55% saw home values climb in April from March. Of the 30 biggest markets, Sacramento experienced the largest monthly increase, with home values rising 3.4%. Other areas that experienced an uptick in home prices during this time period include Las Vegas (3%) and San Francisco (2.8%).

Meanwhile, over the last year, 29 major markets had a surge in home values, with more than half up by double-digit percentages. Phoenix had the largest increase in home prices, up 25.5%, followed by Sacramento (25.4%), San Francisco (24.8%) and Las Vegas (23%). The only major city tracked by Zillow where home values declined year-over-year was Chicago.

However, national rents declined 0.2% in April from the prior month with the index now at $1,288. But rents were still up 3.9% from a year ago.

“In the short term, this has been welcome news for homeowners. But in the long term, this cannot be sustained, and consumers entering the market today should not expect this kind of appreciation to last,” said Stan Humphries, chief economist for Zillow.

For example, starting in April 2013, Zillow is predicting for only a 4% rise in home values for the next 12 months to approximately $164,648. This represents a decrease from 5.2% annual rate of appreciation recorded between April 2012 and the present time.

“Overall, we expect home value appreciation to moderate as more supply comes on line over the next year, but in some areas, runaway home value appreciation, combined with expected interest rate hikes in coming years, runs a real risk of pricing out many potential buyers,” Humphries added. “Home values in these areas will have to flatten or even fall to come back in line.”

Home Price Increases are Robust and are likely to Stay that Way

CoreLogic has released a new analysis of home price trends that finds prices increased by 7.3% in 2012, the strongest rate of appreciation in nearly seven years. The data draws from the CoreLogic Case-Shiller Indexes, which cover more than 380 U.S. markets. The analysis also projected that the trend of rising home prices will continue in 2013 and beyond. In the five-year period from the fourth quarter of 2012 to the fourth quarter of 2017, home prices are expected to rise at an annualized rate of 3.9%, the company says.

“Home prices were up in seven out of every 10 metro areas in 2012. By comparison, in 2011, prices appreciated in fewer than one in five markets,” says Dr. David Stiff, chief economist for CoreLogic Case-Shiller. “We expect strong buying activity this spring will lead to stabilization of home prices in most lagging markets, resulting in rising home prices in nearly every metro area by the end of 2013.”

The largest year-over-year price gains were recorded in many of the metro areas that were at the epicenter of the housing bubble/crash, including Phoenix (24%), Miami (14%) and Las Vegas (13%). In addition, price declines moderated in metro areas with lagging recoveries, such as Long Island, N.Y. (-4%), Virginia Beach, Va., (-2%) and Philadelphia (-1%).

The data point to continuing price appreciation, but the overall national rate of home price increases in 2013 is projected to decelerate from 2012 levels. The CoreLogic Case-Shiller Indexes project a 2.5% home price increase in 2013, as the market dynamic shifts again in bubble/crash metro areas.

While homes in these markets are still significantly undervalued, the strong investor demand for foreclosed properties, record levels of housing affordability and other demand factors that have driven recent double-digit price gains are unlikely to persist throughout the year. In addition, as prices rebound, more existing homes will be listed for sale, particularly those of homeowners who had negative equity prior to the recent price jump. Price appreciation will also be limited by the increase in supply as more new homes are built.

The FHFA says that housing prices nationwide rose by 1.3% in March from February and rose 7.2% year-over-year.

New home sales for April rose to 454K, beating consensus estimates of 425K. March sales were revised higher to 444K from 417K.

Economic News

Jobless claims in the U.S. reversed back down, falling by 23,000 filings for the week ending May 18 and hitting 340,000 total claims. This slight increase comes after last week’s revised figure of 363,000, according to the Department of Labor. The four-week moving average was 339,500, a drop of 500 filings from the previous week. Analysts with Econoday said there have been a few bright spots on the outlook for May’s economic data. “This report is definitely a strong positive for the employment outlook. Whether this correlates with gains for the Dow is uncertain given the possibility, following yesterday’s hawkish sounding FOMC minutes, that strong data could begin to trigger withdrawal of Federal Reserve stimulus,” Econoday said.

Sources: CNBC,Housingwire, Mortgage.orb, Bloomberg, MMG, Origination News